What is the 537 Installment Sale Trust?

A 537 Installment Sale Trust (537 IST) is a trust arrangement that combines special-purpose vehicles with installment sales. This financial strategy is commonly used in property transactions, especially for business sales, to defer capital gains tax over time. When structured correctly, assets can grow from the entire principal amount sold to the trust, growing from the returns earned on taxes you deferred. This deferral can go on for generations.

Income is the primary goal of the IST. We can maximize income by deferring the tax, then compounding growth and return from the deferred taxes. With this strategy, we can yield additional returns from cash that would have otherwise been subject to capital gains tax.

First used by Ernst & Ernst (Ernst & Young) for internal clients in 1971, the IST method has been around for decades. The 537 Installment Sale Trust strategy is 100% IRS Compliant:

- Untaxed on the way in

- Investment Growth

- Taxed as Income, Gains, or Basis on the way out

The 537 Installment Sale Trust uses IRS Code Section 453 and IRS Publication 537 with assets secured in a Business Purpose Trust. The idea behind this strategy is to defer the taxes. Since proceeds go into the trust instead of your bank account, there is no constructive receipt. Thus, no 'taxable event'.

This method allows you to push the recognition of your gains from the sale into future tax years, when you receive the payments. If you sold a property that increased in value over time, you only report and pay tax on the gains you received in the current tax year.

Additionally, cash within the trust is invested for a return, and cash liquidity for other investments without the complexities and timelines of a 1031 Exchange. For this reason, it poses a great alternative to a 1031 Exchange.

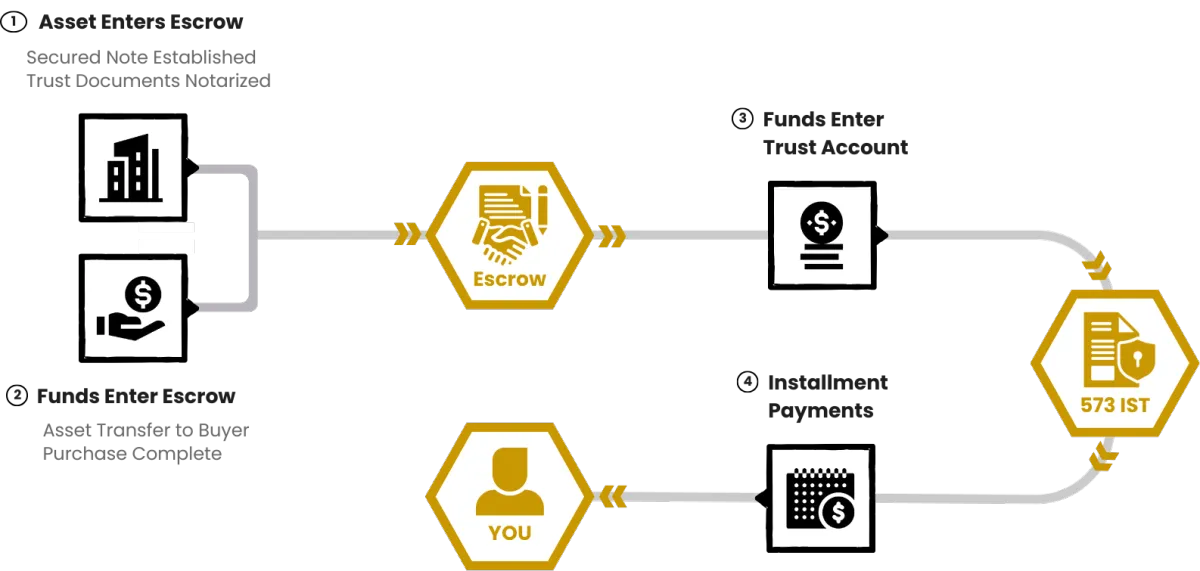

How Does a 537 Installment Sale Trust Work?

Step 1: Our team administers the 537 IST and creates terms for a Secured Note for the seller's protection.

Step 2: At close of escrow, the proceeds directly enter the trust.

Step 3: The Trustee invests proceeds for a significant return aiming at both income and growth.

Step 4: The note pays out quarterly income. From here, the process can continuously be repeated.

Why is the 537 IST Compliant?

The 537 IST defers the Capital Gains Taxes from the transaction. When you receive income from the trust, you pay income tax based on your tax bracket, like any other income.

- No third-party loans: The seller doesn’t “monetize” the note or borrow the proceeds; it’s a genuine installment sale, not a backdoor cash-out.

- No constructive receipt: The seller never touches or borrows the principal deferred. Their only asset on paper is a secured, interest-bearing installment note.

- Full compliance with IRS Publication 537: Every document, transaction, and timeline aligns precisely with Section 453; nothing stretched, nothing skirted, and no gray area.

- Independent fiduciary oversight: Each trust is managed by a licensed, third-party trustee with a fiduciary duty to protect the seller’s interests and ensure regulatory integrity. We ensure compliance by using a third-party trustee service, IST Admin Services.

The assets within the trust can not be directly under your name to avoid constructive receipt, causing taxes owed immediately. The Secured Note and Fiduciary Trustee Service protects your interest entirely. With the Secured Note granted to you, the Note collateralizes the Trust Assets, providing your security.

For additional legal questions, please contact us at +1 (800) 345-9808.

IRC Section 453 – Installment Method

Installment Method Defined: A method of reporting gain from the sale of property where at least one payment is received after the tax year of sale.

Tax Deferral Mechanism: Taxes are only paid as principal is received. You recognize gains proportionally to payments received.

Applicable to:

- Real estate

- Businesses

- Personal property (if eligible)

Publication 537

If any part of the sale proceeds is received after the year of sale, it qualifies as an installment sale. This enables deferral of gain, spreading taxes over the years you receive payments.

Tax is paid only on the gain received. You don't owe tax on the full sale price up front — only on the portion of profit included in each payment.

Each payment is split into:

- Return of basis (non-taxable)

- Gain (profit) (taxable)

Benefits of a 537 IST

Tax-Deferred Growth

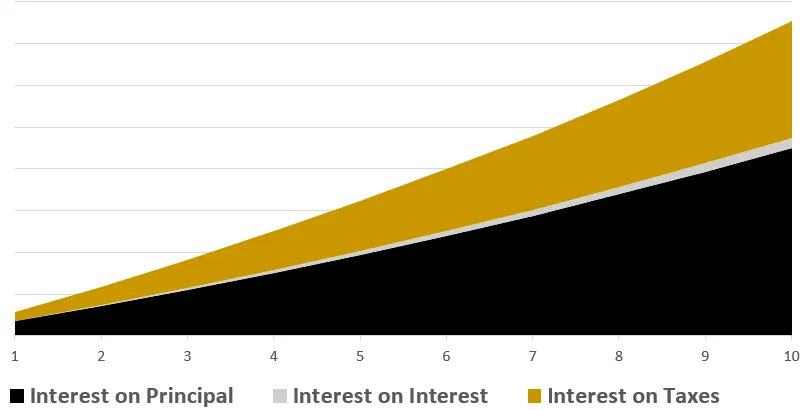

When you sell an asset using a 537 IST, the proceeds are received by the Trust and invested by the Trustee. Taxes on the gains are deferred, not eliminated, until you receive distributions. This deferral allows the invested principal to grow uninterrupted by immediate taxation. This creates the potential for compounding growth across three levels:

1. Interest on Principal: This is the most straightforward level of compounding. The principal is invested, and the returns or interest from this investment are added back to the principal, thus increasing the total amount of money that can earn interest.

2. Interest on Interest: As the interest from the principal is reinvested and generates its interest, a second layer of compounding is required. Over time, this can significantly increase the growth of the investment.

3. Interest on Taxes Deferred: Because the money in the 537 IST is not immediately taxed, the amount that would have gone towards taxes is instead earning interest. This is another layer of compounding, allowing the funds that would have been lost to taxes to contribute to the overall growth of the Trust.

By utilizing these three layers of compounding interest, a 537 Installment Sale Trust can help the proceeds from a sale grow significantly over time, maximizing the benefit of tax deferral.

Guaranteed Income

One of the most appealing aspects of the 537 Installment Sale Trust is the income it generates. Since the 537 uses an interest-only note, cash received is treated as interest income. This means you are not realizing the principal invested.

As the Note Holder, you continue to receive payments in strenuous market conditions. Even if markets are fluctuating, we maintain note payments through the FIA to prevent a realized loss on the funds exposed to the market. Income is guaranteed at 6% of the original, pre-tax, trust value per year; however, this rate does not include the additional growth that stays inside the trust, compounding.

The income from a 537 Installment Sale Trust is designed to be both secured and predictable.

The secured promissory note received from the trust outlines the payment terms. This note is backed by the trust’s portfolio, meaning all assets held within the trust serve as collateral for the payments owed. If payments were ever missed, the note holder has a lien over those assets, similar to a lender’s position on a mortgage. This legal claim ensures that the noteholder is backed by tangible value, rather than mere promises.

Asset Protection & Security

A Secured Note is a financial instrument that represents a promise to pay, but with a crucial safeguard: it is backed by specific assets. These assets serve as collateral, ensuring that the holder of the note has a secured claim to repayment.

This functions similarly to how a bank holds your home or car as security for a loan; if the borrower defaults, the lender has the right to those assets. In the context of the 537 Installment Sale Trust, the Trust itself becomes the borrower. It holds the sale proceeds from your asset and invests those funds. The investments within the Trust act as the collateral that secures your installment note. This is the legal promise that you’ll receive your future payments.

Because the trust holds title to the asset, and because the seller typically does not serve as trustee, the asset is no longer directly exposed in the same way as if it were personally owned. Instead, the seller’s interest is limited to the installment note. In certain legal circumstances, that distinction may reduce exposure to future creditor claims, lawsuits, or liability events that arise after the transaction has been completed.

1031 Exchange Safety Net

When selling an investment property, most investors rely on a 1031 Exchange to defer their capital gains taxes. However, 1031 Exchanges come with strict deadlines and qualifying rules. If the exchange fails to close within 180 days or the replacement property cannot be identified, the entire gain can become taxable.

To avoid this outcome, investors may decide to use the 537 IST as a safety net. To achieve this, the accommodation language must state that the proceeds will be directed into a 537 Installment Sale Trust instead of returning to the seller. This prearranged option allows the seller to seamlessly pivot from a 1031 to a 537 installment sale without triggering immediate taxation.

Do you have liquidity?

Many well-known tax-deferral strategies “lock up” your money. 1031 exchanges keep it in real estate, Delaware Statutory Trusts hold it within a portfolio, Structured Installment Sales have surrender fees, and an irrevocable trust structure doesn’t allow the trust to be unwound.

While many traditional methods limit flexibility, the 537 Installment Sale Trust was specifically designed to maintain liquidity and control, giving you access to your capital if or when you need it, without losing the benefits of tax deferral.

Liquidity refers to how easily you can access your funds or convert your investment into cash. In the 537 IST, liquidity is maintained through the secured installment note, which represents your ownership interest in the Trust’s assets.

You are not selling the property directly for cash, but rather exchanging it for a note. Your gain is deferred while the Trust still holds and manages investments on your behalf.

How are the assets invested inside the trust?

Model Q® Investment Strategy

The Model Q® Strategy was inspired by the long-standing “Rule of 100,” a traditional Wall Street guideline that helps investors balance growth and income by allocating assets between stocks and bonds. While that principle remains useful as a baseline, Model Q® expands on it by addressing a critical flaw that traditional allocation models often ignore: systemic risk.

Diversification can manage most forms of market risk, smoothing returns and reducing volatility over time. However, systemic risk, the type that affects the entire financial system, cannot be so easily diversified. This is where most conventional strategies fall short, and where Model Q® sets itself apart.

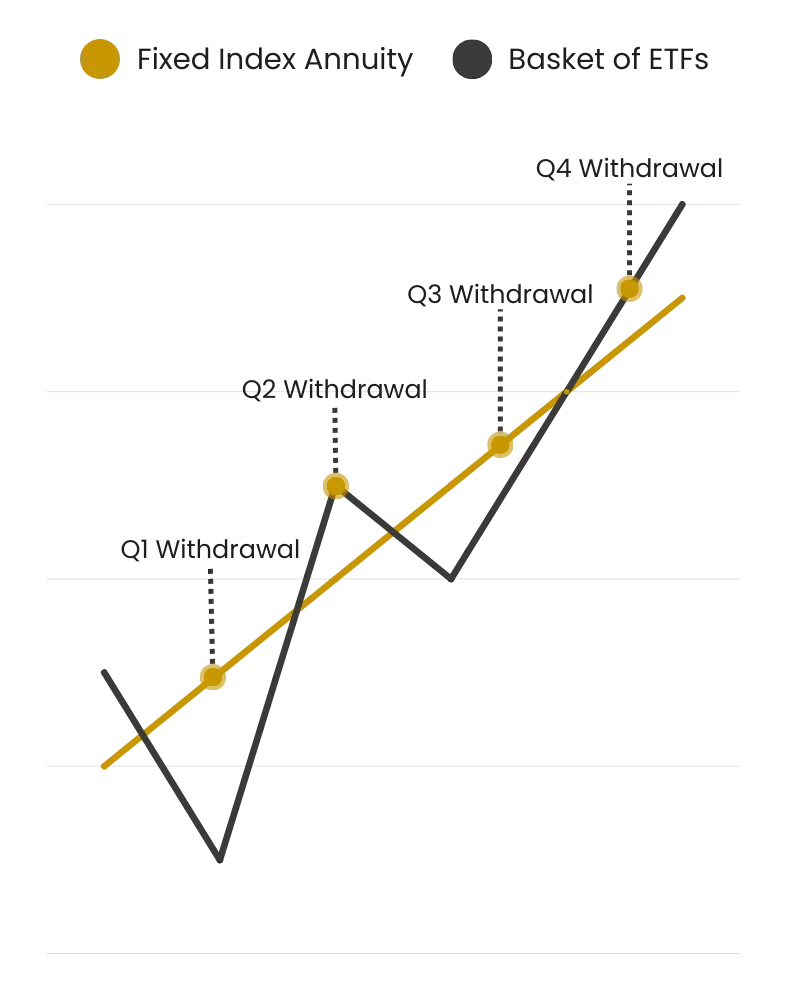

Originally derived from an E.F. Hutton training concept in the 1970s that balanced stock portfolios with fixed annuities, Model Q® uses modern financial instruments such as Exchange-Traded Funds (ETFs) for growth and Principal-Insured Fixed-Indexed Annuities (FIAs) for stability.

By integrating these two components, Model Q® achieves a strategy designed to minimize downside risk, preserve principal, and protect against the sequence-of-returns risk that can derail long-term financial goals.

Money in a 537 IST is managed similarly to a retirement account. All funds are handled through trusted, well-known firms such as Charles Schwab and SEI, and A-rated insurance carriers such as Nationwide, Athene, and Penn Mutual. This structure ensures your assets are safely held and managed by some of the most reputable financial institutions in the country.

Basket of ETFs

A basket of ETFs is a group of exchange-traded funds (ETFs) selected and purchased together as a unit, usually to diversify investments across multiple sectors and asset classes. A basket of ETFs captures the market’s upside potential.

Fixed Index Annuity

A Fixed Indexed Annuity is a long-term insurance solution that offers market-linked growth potential and income options. The original principal is protected from stock market declines and supported by the financial strength of the issuing insurance carrier. The growth rate is capped; however, during market downturns, the FIA provides income stability without depleting market-tied assets. This gives the basket of ETFs time to recover without forced withdrawals at a loss.

537 IST Step up in basis

The 537 IST may be passed on to heirs. When the promissory note is passed on, there may be a step up in basis. This calculation is complex and unique for each situation, we can discuss this with you specifically.

This allows your heir to either take the cash or receive an income stream. This makes the 537 IST an excellent generational wealth tool for succession and estate planning.

Who can Benefit From a 537 IST?

Retirees

The 537 IST is especially popular among retirees seeking to liquidate investment assets while securing a predictable, tax-efficient income stream. By deferring the recognition of capital gains, the 537 IST provides retirees with more clarity over their annual income.

Generational Income Planners

Many families aim to create a lasting income stream for future generations. With the 537 IST, income distributions can be allocated among heirs, enabling generational wealth transfer without depleting the principal. This preserves the core capital while providing ongoing, tax-efficient cash flow across generations.

Real Estate Investors

Real estate investors often face challenges when planning an exit. especially if they’re nearing retirement or their heirs have no interest in managing property. The 537 Installment Sale Trust offers a flexible solution, particularly for those who have heavily depreciated their assets. It allows for a tax-deferred sale without the burden of management or forced inheritance.

Business Sellers

For many business owners, selling a company often triggers a significant capital gains tax, with few alternatives to manage it. The 537 IST offers a powerful option to defer taxes and convert sale proceeds into a structured, predictable income stream. This provides far greater clarity around post-sale retirement income and long-term financial planning.

Empty Nesters

Empty nesters often wish to downsize or relocate, but the potential capital gains tax from selling a long-held property can create hesitation. With the 537 Installment Sale Trust, they now have a way to transition out of their property while deferring taxes and preserving more of their equity. It’s a smart exit strategy that supports lifestyle changes without a sudden tax hit.

Your Next Step: 537 IST Revenue Estimator

Every Revenue Estimator runs an assessment on your asset, showing a variety

of costs and taxes associated with selling an asset. This report outlines:

- Your expected tax liability without the 537 IST

- Interest income generated from deferred taxes

- A Side-by-side comparison to a 1031 exchange and traditional sale

- Hypothetical growth situations based off past market trends

"How The Top 1% Legally Pay $0 Capital Gains Tax On Real Estate"

Watch this interview with our founder, Kevin Brunner, and real estate professional Rod Khleif, where they discuss how the 537 IST works, why someone would consider it, and why it is legal.

537 IST FAQ

"Can I do this with my own Trust and why do I need a Trustee Service?"

No, you cannot use this for your own trust, as that has a different purpose. Additionally, you cannot be the Trustee of the Trust. This would violate the necessary Arms Length and Related Party Doctrine of the tax code. You have extended rights and security as the owner of the promissory note, which fully protects and collateralizes your assets in the Trust.

Similarly to a 1031, where you can't facilitate your own exchange, you cannot facilitate your own 537 Installment Sale Trust. The reason being, there has to be a business purpose outside of solely deferring the taxes for the IRS to consider this a commercially viable transaction.

The Trustee service for the 537 IST transactions can be found here https://istadmin.com/about.

What are the main rules inside the 537 IST to stay compliant?

The 537 IST has a lot of flexibility with the ability to re-enter real estate, defer income, solve debt, invest in stocks, bonds, and more. But there are rules to keep in mind before pulling the trigger.

-The 537 IST cannot invest more than 50% of the funds in one Investment. With having an Accredited Investment Fiduciary manage the money and Fiduciary Trustees, we have a higher level of obligation to you in comparison to your typical advisor or money manager. If we allowed for bad investment decisions and were not diversified, we would lose our licenses and trigger lawsuits, malpractice claims, and more.

But we will happily look into and accept outside investment vehicles as a means of investing the funds inside the 537 IST if they check the right boxes.

-The 537 IST cannot invest funds to purchase a personal residence, asset, or secondary home. Think of it this way: if it is not something generating a return and is something simply for your own personal pleasure, it is not a viable use of funds inside the IST. Doing this could very easily trigger an audit and a taxable event.

-Once you pull out funds, they are taxable to you. Similar to how an LLC operates, the 537 IST is a pass-through entity and comes down to you. You get taxed based on what you extract, so keep that in mind if you decide to pull additional funds outside your income stream.

Does the 537 IST get a step-up in basis like real estate?

Yes. The 537 Installment Sale Trust structure gives you more flexibility and powers on receiving the step-up in basis. The 537 IRS treats the Note you hold against the 537 IST as a Security, and Securities receive a step-up in basis. If you would like more information on this, such as TAMs (Technical Advice Memorandums) or Revenue Rulings, please give us a call so we can email it to you!

Does the 537 IST have a minimum requirement?

Yes, the 537 IST has a minimum requirement of $1,000,000 because of the fee structure being so low. Anything less than that, the fees are not able to cover the expenses that the Trust has with accounting, tax returns, bank accounts, management, and more.

But, if you plan to do more than one transaction inside the 537 Installment Sale Trust, we can start under $1,000,000 and eventually insert the additional capital gains on the next transaction to hit the sum of that number.

Do I need multiple 537 ISTs if I am selling more than one property or business?

No, there is no need for multiple 537 Installment Sale Trusts. Once you have one, you can do an unlimited number of transactions inside. It is going to feel like a Traditional IRA Account with the context that you put income into to defer the income taxes in one account, but in this case, with the 537 IST, it is one Trust account made for capital gains deferral.

How do I know my money is secure?

As the Note Holder, your collateral is all of the assets in the Trust. No money movement or investments can be made without your approval. These Trust accounts have DACA Agreements Authenticator apps, and more security that requires you to approve any investments or withdrawals from the Trust and prevent us from being able to commit fraud or malpractice.

Chances are, this will be the most secure account you've had or will have in your life. We intentionally put all of these security measures in place because if we were on your side of the table, we would expect the same.

Along with this, we have Fidelity Bonds, E&O Insurance, and more that cover your funds in the event that there is malpractice or fraud. If we somehow found a way to convince you to send us all of your money, you would be made whole and more.

Where does the 537 IST come from?

The 537 IST is a variation of the old Ernst & Ernst program, before they became Ernst & Young, that was created to help their partners exit without the capital gains tax liability. This was not a creation of ours, but something that we learned from them and applied to our own business. With this model, we have been able to help facilitate 3800+ transactions in over 20 years.

The Installment Sale Method is the backbone for Mergers and Acquisitions deals and has been a staple for large companies such as FedEx to help their line haul route owners sell their routes with preferred terms and no capital gains tax liability due at close.

What happens if I get audited?

We have never had an audit in the years we have been doing business, but, in the event that there was one, we would represent you. We have Tax Attorneys, CPAs, and more professionals that back this strategy, along with IRS Revenue Rulings and Technical Advice Memorandums to base our defense on.

There is no cost associated with us defending you. That is fixed in your Trust administration fee.

Our philosophy is to communicate with the IRS, not hide from them. We do our best to have annual conversations with IRS auditors and ensure that we are facilitating the 537 IST in a compliant fashion and staying outside of any 'gray areas.'

Do I have to perform a carry back or seller financing for the property/business?

No, the 537 IST does not need to perform any carry back or seller financing like a typical Installment Sale. The entirety of the proceeds land inside the 537 Installment Sale Trust, and you can opt in to receiving Installment Payments from the interest accrued or deferring the payments inside the Trust.

Depending on the transaction, we can perform a carry back with the 537 Installment Sale Trust. This is a case-by-case situation and must be discussed with an IST advisor.

Kevin Brunner is a Best-Selling Author of “Just Say No To Bad Financial Advice”, a Marine Corps veteran, and a seasoned entrepreneur with over 30 years of experience helping businesses grow—from startups to turnarounds.

With two decades in financial services and a special focus on doctors and business owners, Kevin brings real-world insight to every client relationship.

He’s owned a national business brokerage and has been involved in over 3,800 transactions, giving him a deep understanding of both what to do—and what not to do. His core belief: retirement is about income, not assets, because not all assets produce the same results.

Kevin’s been featured in Forbes, hosted The Smart Money Hour on KABC, and today leads a multidisciplinary team of advisors, CPAs, and attorneys specializing in retirement income, tax planning, business strategy, and wealth preservation.

A world traveler to 47 countries, Kevin is passionate about sharing the lessons and blessings he’s gained along the way. He’s also the founder of The Q Companies, which includes Q-RIA.com, Q-1031.com, Q-Hedge.com, TaxFreeYou.com, SellYourBusinessNow.com, SellMyFDX.com, and fiduciary entities like CB Administrative Services and IST Admin Services.

Nothing on this site should be interpreted to state or imply that past results are an indication of future performance. This site does not constitute a complete description of our investment services and is for informational purposes only. It is in no way a solicitation or an offer to sell insurance, annuities, securities or investment advisory services except, where applicable, in states where we are registered or where an exemption or exclusion from such registration or licensing exists. Information throughout this internet site, whether stock quotes, charts, articles, or any other statements regarding market or other financial information, is obtained from sources which we, and our suppliers believe reliable, but we do not warrant or guarantee the timeliness or accuracy of this information. Neither our information providers nor we shall be liable for any errors or inaccuracies, regardless of cause, or the lack of timeliness of, or for any delay or interruption in the transmission thereof to the user. All investments involve risk, including foreign currency exchange rates, political risks, different methods of accounting and financial reporting, and foreign taxes.